Bullets:

Bond yields in the United States have risen sharply since just five years ago. Lenders and bond investors have paper losses of nearly 20% on its US Treasury portfolios since that time.This poses serious challenges for banks, with large US Treasury holdings. They need their reserves to hold value over time, to capitalize the institution, and to collateralize new loans.China’s banking regulators have instructed their largest banks to cease new purchases of US government debt, and to strongly consider selling existing holdings.The Chinese government itself has slashed its holdings of US Treasury bonds, which are at the lowest level in eighteen years.

Inside China / Business is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Report:

Good morning.

Bond yields and bond prices move in opposite directions, so if the price of a bond goes up, the yield earned by the lender goes down. Borrowers that are more credit-worthy can borrow more money, at lower interest rates, compared to borrowers who are considered higher risk. Lenders, or bond investors, are willing to pay higher prices for debt issued by credit-worthy borrowers, in other words, and that means lower borrowing rates for high-quality debt.

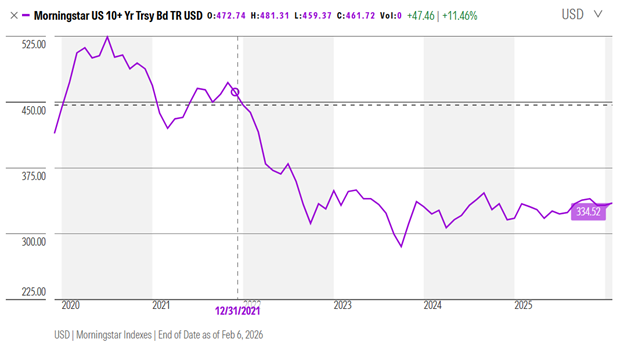

Over the past five years the bond yields on US Treasury debt have risen, sharply. At the beginning of 2022, the US government borrowed money for 10 years at 1.76% per year. Today it’s over 4%, 4.22% as of this morning. Yields have risen, and so when Treasury bonds are priced in dollars, the values are falling:

An investor of 10-year Treasury bonds has seen a drop of 19% in the market value of his bonds over the past four years. That investor has a problem then—if he sells those Treasury bonds, he realizes a loss of nearly 20%. If he holds the bonds to maturity, he will be repaid the principal with inflated dollars that are worth much less than the dollars he used to buy the bonds.

All of this poses serious problems for banks, who need their capital reserves to hold their value over time. Bank reserves are what capitalize the bank, and collateralize new loans for bank customers.

Now, China’s regulators are instructing their financial institutions to limit new purchases of American government bonds; and for the banks that have high exposures to US treasuries to sell them. Last year, China’s banks held $300 billion in dollar-denominated bonds, and lots of those would be US Treasuries or agency paper.

At issue, for China’s banking regulators, is that the underlying Treasury bonds are losing value, and doing so quickly, and that undermines the safe haven status of these instruments. It’s much less about whether the US government will pay their debts; the Fed and Treasury can simply print money to cover interest and principal payments. The problem rather is that the mark-to-market value of the bonds make them risky, to be held as bank reserves.

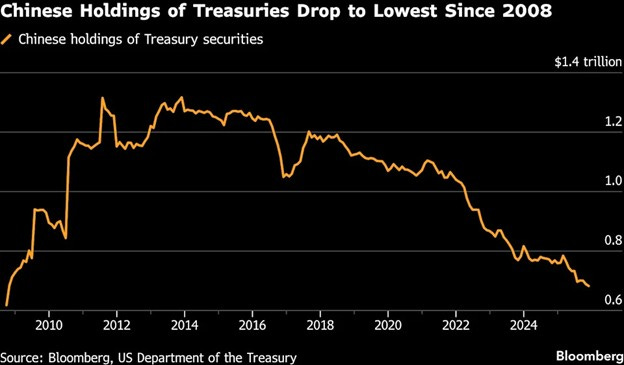

China has slashed its sovereign reserve holdings of US Treasuries, which are now at the lowest level in almost 20 years. These are Treasury bond holdings of the Chinese government itself, and the People’s Bank of China. The BRICS countries are building a new financial system outside Western banks, and Western currencies, and are capitalizing that new system with dollars already in their own banking systems, with their own national currencies, and with gold.

This point is important:

These instructions to Chinese banks are not yet in writing; they’re not yet codified into hard regulation. That gives the banks some time and flexibility to handle the unwinding of their US Treasury holdings. But at any time in the future, bank regulators can officially change what they recognize as bank reserves, which are the basis for new loans. Point here is that China’s regulators today are telling their banks to strongly consider selling Treasuring bonds, and definitely not to buy any more. Tomorrow they may say that for the banks who still hold US Treasuries, they cannot include the full market value of them as part of their capital reserves, used to create new loans for new customers. They’re too risky.

Be good.

**Resources and links:**China urges banks to curb US Treasuries exposure, Bloomberg News reportshttps://www.reuters.com/world/asia-pacific/china-urges-banks-curb-us-treasuries-exposure-bloomberg-news-reports-2026-02-09/China Urges Banks to Curb Exposure to US treasurieshttps://www.bloomberg.com/news/articles/2026-02-09/china-urges-banks-to-limit-holdings-of-us-treasuries-citing-market-volatilityTreasuries Fall as China Banks Asked to Limit Bond holdingshttps://finance.yahoo.com/news/treasuries-fall-china-banks-asked-081715745.htmlMarket Yield on U.S. Treasury Securities at 10-Year Constant maturityhttps://fred.stlouisfed.org/series/DGS10Trading View, US Government Bonds 10 YR yieldhttps://www.tradingview.com/symbols/TVC-US10Y/?timeframe=60M

Inside China / Business is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

From Inside China / Business via this RSS feed