Hi! If you like this piece and want to support my independent reporting and analysis, why not subscribe to my premium newsletter? It’s $70 a year, or $7 a month, and in return you get a weekly newsletter that’s usually anywhere from 5000 to 18,000 words, including vast, detailed analyses of NVIDIA, Anthropic and OpenAI’s finances, and the AI bubble writ large. I just put out a massive Hater’s Guide To The SaaSpocalypse, as well as the Hater’s Guide to Adobe. It helps support free newsletters like these!

The entire AI bubble is built on a vague sense of inevitability — that if everybody just believes hard enough that none of this can ever, ever go wrong that at some point all of the very obvious problems will just go away.

Sadly, one cannot beat physics.

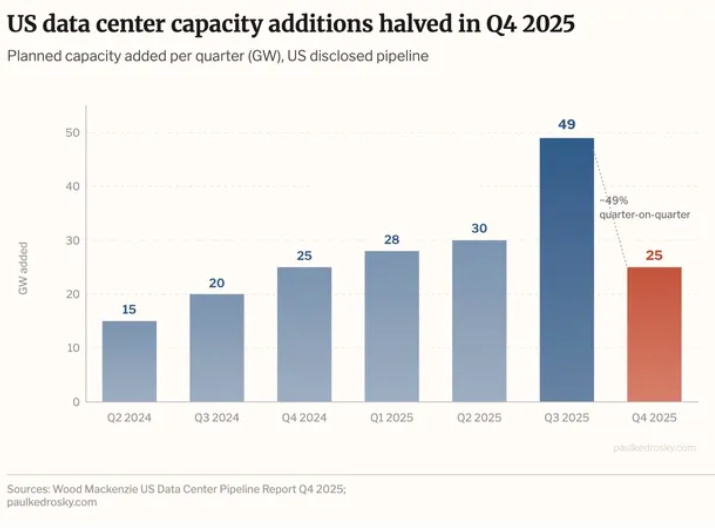

Last week, economist Paul Kedrosky put out an excellent piece centered around a chart that showed new data center capacity additions (as in additions to the pipeline, not brought online) halved in the fourth quarter of 2025 (per data from Wood Mackenzie):

Wood Mackenzie’s report framed it in harsh terms:

US data-centre capacity additions halved from Q3 to Q4 2025 as load-queue challenges persisted. The decline underscores the difficulties of the current development environment and signals a resulting focus on existing pipeline projects. While Texas extended its pipeline capacity lead in Q4 2025, New Mexico, Indiana and Wyoming saw greater relative growth. Planned capacity continues to be weighted by new developers with a small number of massive, speculative projects, targeting in particular the South and Southwest. New Mexico owes its growth to a single, massive, speculative project by New Era Energy & Digital in Lea County.

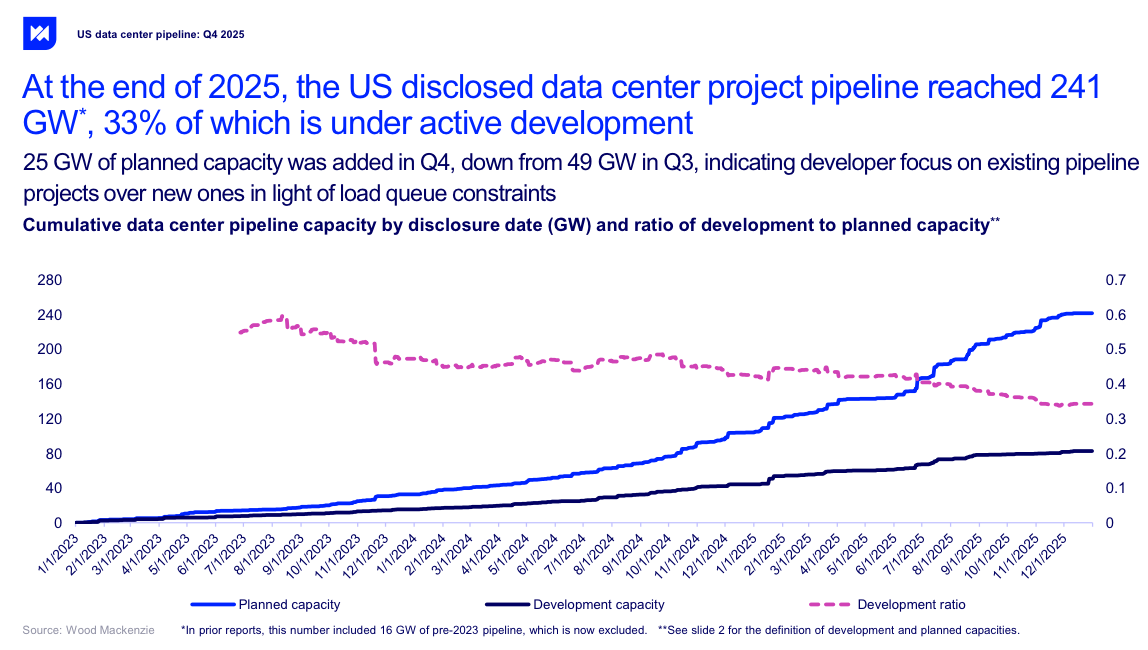

As I said above, this refers only to capacity that’s been announced rather than stuff that’s actually been brought online, and Kedrosky missed arguably the craziest chart — that of the 241GW of disclosed data center capacity, only 33% of it is actually under active development:

The report also adds that the majority of committed power (58%) is for “wires-only utilities,” which means the utility provider is only responsible for getting power to the facility, not generating the power itself, which is a big problem when you’re building entire campuses made up of power-hungry AI servers.

WoodMac also adds that PJM, one of the largest utility providers in America, “…remains in trouble, with utility large load commitments three times as large as the accredited capacity in PJM’s risked generation queue,” which is a complex way of saying “it doesn’t have enough power.”

This means that fifty eight god damn percent of data centers need to work out their own power somehow. WoodMac also adds there is around $948 billion in capex being spent in totality on US-based data centers, but capex growth decelerated for the first time since 2023. Kedrosky adds:

The total announced pipeline looks huge at 241 GW — about twice US peak electricity demand — but most of it is not real. Only a third is under construction, with the rest a mix of hopeful permits, speculative land deals, and projects that assume power sources nobody has actually built yet. In particular, much of it assumes on-site gas plants, a fraught assumption given current geopolitics.The most serious problem is in the mid-Atlantic. Regional grid operator PJM has made power commitments to data centers at roughly three times the rate that new generation is actually coming online. Someone is going to be waiting a very long time, or paying a lot more than they expected, or both.

Let’s simplify:

Only 33% of announced US data centers are actually being built, with the rest in vague levels of “planning.” That’s about 79.53GW of power, or 61GW of IT load. “Active development” also refers to anything that is (and I quote) “…under development or construction,” meaning “we’ve got the land and we’re still working out what to do with it.This is pretty obvious when you do the maths. 61GW of IT load would be hundreds of thousands of NVIDIA GB200 NVL72 racks — over a trillion dollars of GPUs at $3 million per 72-GPU rack — and based on the fact there were only $178.5 billion in data center debt deals last year, I don’t think many of these are actually being built right now.Even if they were, there’s not enough power for them to turn on.NVIDIA claims it will sell $1 trillion of GPUs between 2025 and 2027, and as I calculated previously, it sells about 1.6GW (in IT load terms, as in how much power just the GPUs draw) of GPUs every quarter, which would require at least 1.95GW of power just to run, when you include all the associated gear and the challenges of physically getting power.None of this data talks about data centers actually coming online.

How Much Actual Data Center Capacity Came Online In 2025? My Estimate: 3GW of IT Load

The term you’re looking for there is data center absorption, which is (to quote Data Center Dynamics) “…the net growth in occupied, revenue-producing IT load,” which grew in America’s primary markets from 1.8GW in new capacity in 2024 to 2.5GW of new capacity in 2025 according to CBRE*.*

Definition sidenote! “Colocation” space refers to data center space built that is then rented out to somebody else, versus data centers explicitly built for a company (such as Microsoft’s Fairwater data centers). What’s interesting is that it appears that some — such as Avison Young — count Crusoe’s developments (such as Stargate Abilene) as colocation construction, which makes the collocation numbers I’ll get to shortly much more indicative of the greater picture.

The problem is, this number doesn’t actually express newly-turned-on data centers. Somebody expanding a project to take on another 50MW still counts as “new absorption.”

Things get more confusing when you add in other reports. Avison Young’s reports about data center absorption found 700MW of new capacity in Q1 2025, 1.173GW in Q2, a little over 1.5GW in Q3 and 2.033GW in Q4 (I cannot find its Q3 report anywhere), for a total of 5.44GW, entirely in “colocation,” meaning buildings built to be leased to others.

Yet there’s another problem with that methodology: these are facilities that have been “delivered” or have a “committed tenant.” “Delivered” could mean “the facility has been turned over to the client, but it’s literally a powered shell (a warehouse) waiting for installation,” or it could mean “the client is up and running.” A “committed tenant” could mean anything from “we’ve signed a contract and we’re raising funds” (such as is the case with Nebius raising money off of a Meta contract to build data centers at some point in the future).

We can get a little closer by using the definitions from DataCenterHawk (from whichAvison Young gets its data), which defines absorption as follows:

To measure demand, we want to know how much capacity was leased up by customers over a specific period of time. At datacenterHawk we calculate this quarterly. The resulting number is what’s called absorption.Let’s say DC#1 has 10 MW commissioned. 9 MW are currently leased and 1 MW is available. Over the course of a quarter, DC#1 leases up that last MW to a few tenants. Their absorption for the quarter would be 1 MW. It can get a little more complicated but that’s the basic concept.

That’s great! Except Avison Young has chosen to define absorption in an entirely different way — that a data center (in whatever state of construction it’s in) has been leased, or “delivered,” which means “a fully ready-to-go data center” or “an empty warehouse with power in it.”

CBRE, on the other hand, defines absorption as “net growth in occupied, revenue-producing IT load,” and is inclusive of hyperscaler data centers. Its report also includes smaller markets like Charlotte, Seattle and Minneapolis, adding a further 216MW in absorption of actual new, existing, revenue-generating capacity.

So that’s about 2.716GW of actual, new data centers brought online. It doesn’t include areas like Southern Virginia or Columbus, Ohio — two massive hotspots from Avison Young’s report — and I cannot find a single bit of actual evidence of significant revenue-generating, turned-on, real data center capacity being stood up at scale. DataCenterMap shows 134 data centers in Columbus, but as of August 2025, the Columbus area had around 506MW in total according to the Columbus Dispatch, though Cushman and Wakefield claimed in February 2026 that it had 1.8GW.

Things get even more confusing when you read that Cushman and Wakefield estimates that around 4GW of new colocation supply was “delivered” in 2025, a term it does not define in its actual report, and for whatever reason lacks absorption numbers. Its H1 2025 report, however, includes absorption numbers that add up to around 1.95GW of capacity…without defining absorption, leaving us in exactly the same problem we have with Avison Young.

Nevertheless, based on these data points, I’m comfortable estimating that North American data center absorption — as the IT load of data centers actually turned on and in operation — was at around 3GW for 2025, which would work out to about 3.9GW of total power.

And that number is a fucking disaster.

It Is Currently Taking 6 Months To Install A Quarter of NVIDIA’s GPU Sales, Calling Into Question The Logic of Buying More GPUs

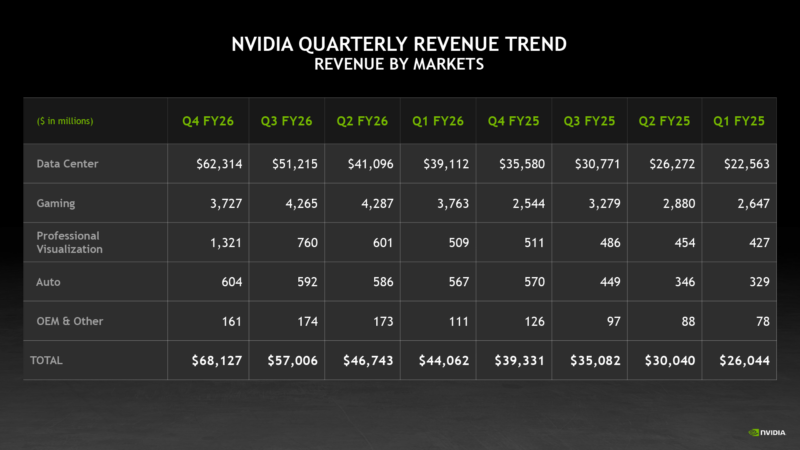

Earlier in the year, TD Cowen’s Jerome Darling told me that GPUs and their associated hardware cost about $30 million a megawatt. 3GW of IT load (as in the GPUs and their associated gear’s power draw) works out to around $90 billion of NVIDIA GPUs and the associated hardware, which would be covered under NVIDIA’s “data center” revenue segment:

America makes up about 69.2% of NVIDIA’s revenue, or around $149.6 billion in FY2026 (which runs, annoyingly, from February 2025 to January 2026). NVIDIA’s overall data center segment revenue was $195.7 billion, which puts America’s data center purchases at around $135 billion, leaving around $44 billion of GPUs and associated technology uninstalled.

With the acceleration of NVIDIA’s GPU sales, it now takes about 6 months to install and operationalize a single quarter’s worth of sales. Because these are Blackwell (and I imagine some of the new next generation Vera Rubin) GPUs, they are more than likely going to new builds thanks to their greater power and cooling requirements, and while some could in theory be going to old builds retrofitted to fit them, NVIDIA’s increasingly-centralized (as in focused on a few very large customers) revenue heavily suggests the presence of large resellers like Dell or Supermicro (which I’ll get to in a bit) or the Taiwanese ODMs like Foxconn and Quanta who manufacture massive amounts of servers for hyperscaler buildouts.

I should also add that it’s commonplace for hyperscalers to buy the GPUs for their colocation partners to install, which is why Nebius and Nscale and other partners never raise more than a few billion dollars to cover construction costs.

It’s becoming very obvious that data center construction is dramatically slower than NVIDIA’s GPU sales, which continue to accelerate dramatically every single quarter.

Even if you think AI is the biggest most hugest and most special boy: what’s the fucking point of buying these things two to four years in advance? Jensen Huang is announcing a new GPU every year!

By the time they actually get all the Blackwells in Vera Rubin will be two years old! And by the time we install those Vera Rubins, some other new GPU will be beating it!

There Is Only 5GW of Global Data Center Capacity Actually Under Construction, And Every Huge, Multi-Gigawatt Project You Read Is Going To Take 2 to 4 Years Or More To Complete — And Wood Mackenzie Believes Capex Growth Will Slow In 2026

Before we go any further, I want to be clear how difficult it is to answer the question “how long does a data center take to build?”. You can’t really say “[time] per megawatt” because things become ever-more complicated with every 100MW or so. As I’ll get into, it’s taken Stargate Abilene two years to hit 200MW of power.

Not IT load. Power.

Anyway, the question of “how much data center capacity came online?” is pretty annoying too.

Sightline’s research — which estimated that “almost 6GW of [global data center power] capacity came online last year” — found that while 16GW of capacity was slated to come online in 2026 across 140 projects, only 5GW is currently under construction, and somehow doesn’t say that “maybe everybody is lying about timelines.”

Sightline believes that half of 2026’s supposed data center pipeline may never materialize, with 11GW of capacity in the “announced” stage with “…no visible construction progress despite typical build timelines of 12-18 months.” “Under construction” also can mean anything from “a single steel beam” to “nearly finished.”

These numbers also are based on 5GW of capacity, meaning about 3.84GW of IT load, or about $111.5 billion in GPUs and associated gear, or roughly 57.5% of NVIDIA’s FY2026 revenue that’s actually getting built.

Sightline (and basically everyone else) argues that there’s a power bottleneck holding back data center development, and Camus explains that the biggest problem is a lack of transmission capacity (the amount of power that can be moved) and power generation (creating the power itself):

The biggest driver of delay is simple: our power system doesn’t have enough extra transmission capacity and generation to serve dozens of gigawatts of new, high-utilization demand 100% of the time. Data centers require round-the-clock power at levels that rival or exceed the needs of small cities, and building new transmission infrastructure and generation requires years of permitting, land acquisition, supply chain management, and construction.

Camus adds that America also isn’t really prepared to add this much power at once:

Inside utilities, planners and engineers are working diligently to connect new loads. But the tools available to planners were built for extending power lines to new neighborhoods or upgrading equipment as communities grow. They weren’t designed to analyze 50 new service requests of 100 MW each, all while new generation applications pile up.As a result, planners and engineers are overwhelmed; they’re stuck working to review new applications while simultaneously configuring new tools that are better equipped for the scale of this challenge. And unlike generation interconnection, which has well-defined steps across most ISOs and utilities, the process for evaluating large loads is often much more ad hoc. This makes adopting the right tools much more difficult too. In fact, the majority of utilities and ISO/RTOs are still developing formal study procedures.

Nevertheless, I also think there’s another more-obvious reason: it takes way longer to build a data center than anybody is letting on, as evidenced by the fact that we only added 3GW or so of actual capacity in America in 2025. NVIDIA is selling GPUs years into the future, and its ability to grow, or even just maintain its current revenues, depends wholly on its ability to convince people that this is somehow rational.

Let me give you an example. OpenAI and Oracle’s Stargate Abilene data center project was first announced in July 2024 as a 200MW data center. In October 2024, the joint venture between Crusoe, Blue Owl and Primary Digital Infrastructure raised $3.4 billion, with the 200MW of capacity due to be delivered “in 2025.” A mid-2025 presentation from land developer Lancium said it would have “1.2GW online by YE2025.” In a May 2025 announcement, Crusoe, Blue Owl, and Primary Digital Infrastructure announced the creation of a $15 billion joint vehicle, and said that Abilene would now be 8 buildings, with the first two buildings being energized by the “first half of 2025,” and that the rest would be “energized by mid-2026.” Each building would have 50,000 GPUs, and the total IT load is meant to be 880MW or so, with a total power draw of 1.2GW.

I’m not interested in discussing OpenAI not taking the supposedly-planned extensions to Abilene because it never existed and was never going to happen.

In December 2025, Oracle stated that it had “delivered” 96,000 GPUs, and in February, Oracle was still only referring to two buildings, likely because that’s all that’s been finished. My sources in Abilene tell me that Building Three is nearly done, but…this thing is meant to be turned on in mid-2026. Developer Mortensen claims the entire project will be completed by October 2026, which it obviously, blatantly won’t.

The AI Industry Is Trying To Hide The Incredibly Slow Growth of Data Centers, And Is Using The Media To Do So

I hate to speak in conspiratorial terms, but this feels like a blatant coverup with the active participation of the press. CNBC reported in September 2025 that “the first data center in $500 billion Stargate project is open in Texas,” referring to a data center with an eighth of its IT load operational as “online” and “up and running,” with Crusoe adding two weeks later that it was “live,” “up and running” and “continuing to progress rapidly,” all so that readers and viewers would think “wow, Stargate Abilene is up and running” despite it being months if not years behind schedule.

At its current rate of construction, Stargate Abilene will be fully built sometime in late 2027. Oracle’s Port Washington Data Center, as of March 6 2026, consisted of a single steel beam. Stargate Shackelford Texas broke ground on December 15 2025, and as of December 2025, construction barely appears to have begun in Stargate New Mexico. Meta’s 1GW data center campus in Indiana only started construction in February 2026.

And, despite Microsoft trying to mislead everybody that its Wisconsin data center had ‘arrived” and “been built,” looking even an inch deeper suggests very little has actually come online” — and, considering the first data center was $3.3 billion (remember: $14 million a megawatt just for construction), I imagine Microsoft has successfully brought online about 235MW of power for Fairwater.

What Microsoft wants you to think is it brought online gigawatts of power (always referred to in the future tense), because Microsoft, like everybody else, is building data centers at a glacial pace, because construction takes forever, even if you have the power, which nobody does!

The concept of a hundred-megawatt data center is barely a few years old, and I cannot actually find a built, in-service gigawatt data center of any kind, just vague promises about theoretical Stargate campuses built for OpenAI, a company that cannot afford to pay its bills.

Everybody keeps yammering on about “what if data centers don’t have power” when they should be thinking about whether data centers are actually getting built. Microsoft proudly boasted in September 2025 about its intent to build “the UK’s largest supercomputer” in Loughton, England with Nscale, and as of March 2026, it’s literally a scaffolding yard full of pylons and scrap metal. Stargate Abilene has been stuck at two buildings for upwards of six months.

Here’s what’s actually happening: data center deals are being funded by eager private credit gargoyles that don’t know shit about fuck. These deals are announced, usually by overly-eager reporters that don’t bother to check whether the previous data centers ever got built, as massive “multi-gigawatt deals,” and then nobody follows up to check whether anything actually happened.

All that anybody needs to fund one of these projects is an eager-enough financier and a connection to NVIDIA. All Nebius had to do to raise $3.75 billion in debt was to sign a deal with Meta for data center capacity that doesn’t exist and will likely take three to four years to build (it’s never happening). Nebius has yet to finish its Vineland, New Jersey data center for Microsoft, which was meant to be “at 100MW” by the end of 2025, but appears to have only had 50MW (the first phase) available as of February 2026.

I’m just gonna come out and say it: I think a lot of these data center deals are trash, will never get built, and thus will never get paid. The tech industry has taken advantage of an understandable lack of knowledge about construction or power timelines in the media to pump out endless stories about “data center capacity in progress” as a means of obfuscating an ever-growing scandal: that hundreds of billions of NVIDIA GPUs got sold to go in projects that may never be built.

These things aren’t getting built, or if they’re getting built, it’s taking way, way longer than expected, which means that interest on that debt is piling up. The longer it takes, the less rational it becomes to buy further NVIDIA GPUs — after all, if data centers are taking anywhere from 18 months to three years to build, why would you be buying more of them? Where are you going to put them, Jensen?

This also seriously brings into question the appetite that private credit and other financiers have for funding these projects, because much of the economic potential comes from the idea that these projects get built and have stable tenants. Furthermore, if the supply of AI compute is a bottleneck, this suggests that when (or if) that bottleneck is ever cleared, there will suddenly be a massive supply glut, lowering the overall value of the data centers in progress…which are, by the way, all filled with Blackwell GPUs, which will be two or three-years-old by the time the data centers are finally turned on.

That’s before you get to the fact that the ruinous debt behind AI data centers makes them all remarkably unprofitable, or that their customers are AI startups that lose hundreds of millions or billions of dollars a year, or that NVIDIA is the largest company on the stock market, and said valuation is a result of a data center construction boom that appears to be decelerating and even if it wasn’t operating at a glacial pace compared to NVIDIA’s sales.

Not to sound unprofessional or nothing, but what the fuck is going on? We have 241GW of “planned” capacity in America, of which only 79.5GW of which is “under active development,” but when you dig deeper, only 5GW of capacity is actually under construction?

The entire AI bubble is a god damn mirage. Every single “multi-gigawatt” data center you hear about is a pipedream, little more than a few contracts and some guys with their hands on their hips saying “brother we’re gonna be so fuckin’ rich!” as they siphon money from private credit — and, by extension, you, because where does private credit get its capital from? That’s right. A lot comes from pension funds and insurance companies.

Here’s the reality: data centers take forever. Every hyperscaler and neocloud talking about “contracted compute” or “planned capacity” may as well be telling you about their planned dinners with The Grinch and Godot. The insanity of the AI buildout will be seen as one of the largest wastes of capital of all time (to paraphrase JustDario), and I anticipate that the majority of the data center deals you’re reading about simply never get built.

The fact that there’s so much data about data center construction and so little data about completed construction suggests that those preparing the reports are in on the con. I give credit to CBRE, Sightline and Wood Mackenzie for having the courage to even lightly push back on the narrative, even if they do so by obfuscating terms like “capacity” or “power” in ways that reporters and other analysts are sure to misinterpret.

Hundreds of billions of dollars have been sunk into buying GPUs, in some cases years in advance, to put into data centers that are being built at a rate that means that NVIDIA’s 2025 and 2026 revenues will take until 2028 to 2029 to actually operationalize, and that’s making the big assumption that any of it actually gets built.

I think it’s also fair to ask where the money is actually going. 2025’s $178.5 billion in US-based data center deals doesn’t appear to be resulting in any immediate (or even future) benefit to anybody involved.

I also wonder whether the demand actually exists to make any of this worthwhile, or what people are actually paying for this compute.

If we assume 3GW of IT load capacity was brought online in America, that should (theoretically) mean tens of billions of dollars of revenue thanks to the “insatiable demand for AI” — except nobody appears to be showing massive amounts of revenue from these data centers.

Applied Digital only had $144 million in revenue in FY2025 (and lost $231 million making it). CoreWeave, which claimed to have “850MW of active power (or around 653MW of IT load)” at the end of 2025 (up from 420MW in Q1 FY2025, or 323MW of IT load), made $5.13 billion of revenue (and lost $1.2 billion before tax) in FY2025.

Nebius? $228 million, for a loss of $122.9 million on 170MW of active power (or around 130MW of IT load). Iren lost $155.4 million on $184.7 million last quarter, and that’s with a release of deferred tax liabilities of $182.5 million. Equinix made about $9.2 billion in revenue in its last fiscal year, and while it made a profit, it’s unclear how much of that came from its large and already-existent data center portfolio, though it’s likely a lot considering Equinix is boasting about its “multi-megawatt” data center plans with no discussion of its actual capacity.

And, of course, Google, Amazon, and Microsoft refuse to break out their AI revenues. Based on my reporting from last year, OpenAI spent about $8.67 billion on Azure through September 2025, and Anthropic around $2.66 billion in the same period on Amazon Web Services. As the two largest consumers of AI compute, this heavily suggests that the actual demand for AI services is pretty weak, and mostly taken up by a few companies (or hyperscalers running their own services.)

At some point reality will set in and spending on NVIDIA GPUs will have to decline. It’s truly insane how much has been invested so many years in the future, and it’s remarkable that nobody else seems this concerned.

Simple questions like “where are the GPUs going?” and “how many actual GPUs have been installed?” are left unanswered as article after article gets written about massive, multi-billion dollar compute deals for data centers that won’t be built before, at this rate, 2030.

And I’d argue it’s convenient to blame this solely on power issues, when the reality is clearly based on construction timelines that never made any sense to begin with. If it was just a power issue, more data centers would be near or at the finish line, waiting for power to be turned on. Instead, well-known projects like Stargate Abilene are built at a glacial pace as eager reporters claim that a quarter of the buildings being functional nearly a year after they were meant to be turned on is some sort of achievement.

Then there’s the very, very obvious scandal that NVIDIA, the largest company on the stock market, is making hundreds of billions of dollars of revenue on chips that aren’t being installed. It’s fucking strange, and I simply do not understand how it keeps beating and raising expectations every quarter given the fact that the majority of its customers are likely going to be able to use their current purchases in the next decade.

Assuming that Vera Rubin actually ships in 2026, it’s reasonable to believe that people will be installing these things well into 2028, if not further, and that’s assuming everything doesn’t collapse by then. Why would you bother? What’s the point, especially if you’re sitting on a pile of Blackwell GPUs?

Why are we doing any of this?

Jensen, How Do All These NVIDIA GPUs Keep Getting To China?

Last week also featured a truly bonkers story about Supermicro, a reseller of GPUs used by CoreWeave and Crusoe, where co-founder Wally Liaw and several other co-conspirators were arrested for selling hundreds of millions of dollars of NVIDIA GPUs to China, with the intent to sell billions more.

Liaw, one of Supermicro’s co-founders, previously resigned in a 2018 accounting scandal where Supermicro couldn’t file its annual reports, only to be (per Hindenburg Research’s excellent report) rehired in 2021 as a consultant, and restored to the board in 2023, per a filed 8K.

Mere days before his arrest, Liaw was parading around NVIDIA’s GTC conference, pouring unnamed liquids in ice luges and standing two people away from NVIDIA CEO Jensen Huang. Liaw was also seen congratulating the CEO of Lambda on its new CFO appointment on LinkedIn, as well as shaking hands (along with Supermicro CEO Charles Liang, who has not been arrested or indicted) with Crusoe (the company building OpenAI’s Abilene data center) CEO Chase Lochmiller.

Supermicro isn’t named in the indictment for reasons I imagine are perfectly normal and not related to keeping the AI party going. Nevertheless, Liaw and his co-conspirators are accused of shipping hundreds of millions of dollars’ worth of NVIDIA GPUs to China through a web of counterparties and brokers, with over $510 million of them shipped between April and mid-May 2025. While the indictment isn’t specific as to the breakdown, it confirms that some Blackwell GPUs made it to China, and I’d wager quite a few.

The mainstream media has already stopped thinking about this story, despite Supermicro being a huge reseller of NVIDIA gear, contributing billions of dollars of revenue, with at least $500 million of that apparently going to China. The fact that Supermicro wasn’t specifically named in the case is enough to erase the entire tale from their minds, along with any wonder about how NVIDIA, and specifically Jensen Huang, didn’t know.

This also isn’t even close to the only time this has happened. Late last year, Bloomberg reported on Singapore-based Megaspeed — a (to quote Bloomberg) “once-obscure spinoff of a Chinese gaming enterprise [that] evolved into the single largest Southeast Asian buyer of NVIDIA chips” — and highlighted odd signs that suggest it might be operating as a front for China.

As a neocloud, Megaspeed rents out AI compute capacity like CoreWeave, and while NVIDIA (and Megaspeed) both deny any of their GPUs are going to China, Megaspeed, to quote Bloomberg, has “something of a Chinese corporate twin”:

This firm used similar presentation materials to Megaspeed’s, had a nearly identical website to a Megaspeed sub-brand and claimed Megaspeed’s Southeast Asia employees as its own. It’s also posted job ads at and near the Shanghai data center whose rendering was used in Megaspeed’s investor deck — including for engineering work on restricted Nvidia GPUs.

Bloomberg reported that Megaspeed imported goods “worth more than a thousand times its cash balance in 2023,” with two-thirds of its imports being NVIDIA products. The investigation got weirder when Bloomberg tried to track down specific circuit boards that NVIDIA had told the US government were in specific sites:

Data centers aren’t the only Megaspeed facilities Nvidia visited. The vast majority of Megaspeed’s $2.4 billion worth of Bianca boards, the circuit boards that house Nvidia’s top-end GB200 and GB300 semiconductors, were unaccounted for at the sites Nvidia described to Washington. After Bloomberg asked about those products, the chipmaker went to separate Megaspeed warehouses, an Nvidia official said, and confirmed the Bianca boards are there.This person declined to specify the number observed in storage, nor where and when the chips — imported more than half a year ago — would be put to use. “Building data centers is a complex process that takes many months and involves many suppliers, contractors and approvals,” an Nvidia spokesperson said.

Things get weirder throughout the article, with a Chinese company called “Shanghai Shuoyao” having a near-identical website and investor deck (as mentioned) to Megaspeed, with several of the “computing clusters under construction” actually being in China.

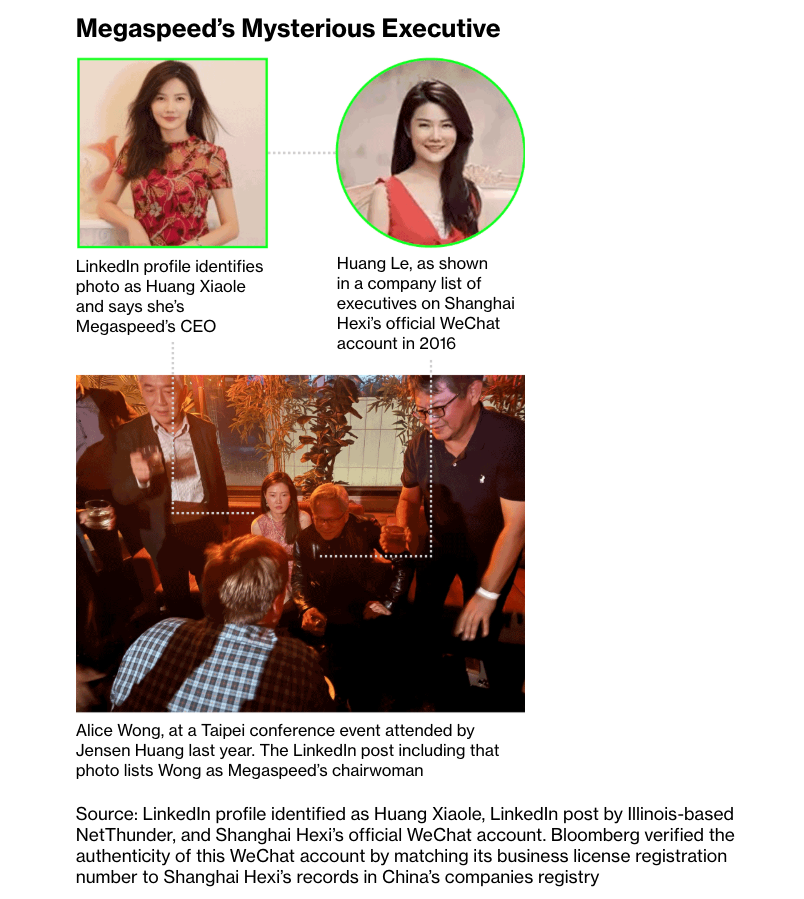

Things get a lot weirder as Bloomberg digs in, including a woman called “Huang” that may or may not be both the CEO of Megaspeed and an associated company called “Shanghai Hexi,” which is also owned by the Yangtze River Delta project… who was also photographed sitting next to Jensen Huang at an event in Taipei in 2024.

While all of this is extremely weird and suspicious, I must be clear there is no declarative answer as to what’s going on, other than that NVIDIA GPUs are absolutely making it to China, somehow. I also think that it would be really tough for Jensen Huang to not know about it, or for billions of dollars of GPUs to be somewhere without NVIDIA’s knowledge.

Anyway, Supermicro CEO Charles Liang has yet to comment on Wally Liaw or his alleged co-conspirators, other than a statement from the company that says that their acts were “a contravention of the Company’s policies and compliance controls.”

Jensen Huang does not appear to have been asked if he knew anything about this — not Megaspeed, not Supermicro, or really any challenging question of any kind for the last few years of his life.

Huang did, however, say back in May 2025 that there was “no evidence of any AI chip diversion,’ and that the countries in question “monitor themselves very carefully.”

[Content truncated due to length…]

You must log in or # to comment.